An exploration into ZK-Rollups & how StarkWare is using them.

Before understanding ZK-Rollups, we need to begin with Layer 2s:

Layer 2s refers to secondary chains built on top of the main, existing blockchain. Their main goal is to solve the scalability problem faced by the main blockchain.

Case Studies:

- Bitcoin Lightning Network for Bitcoin.

- Optimism for Ethereum.

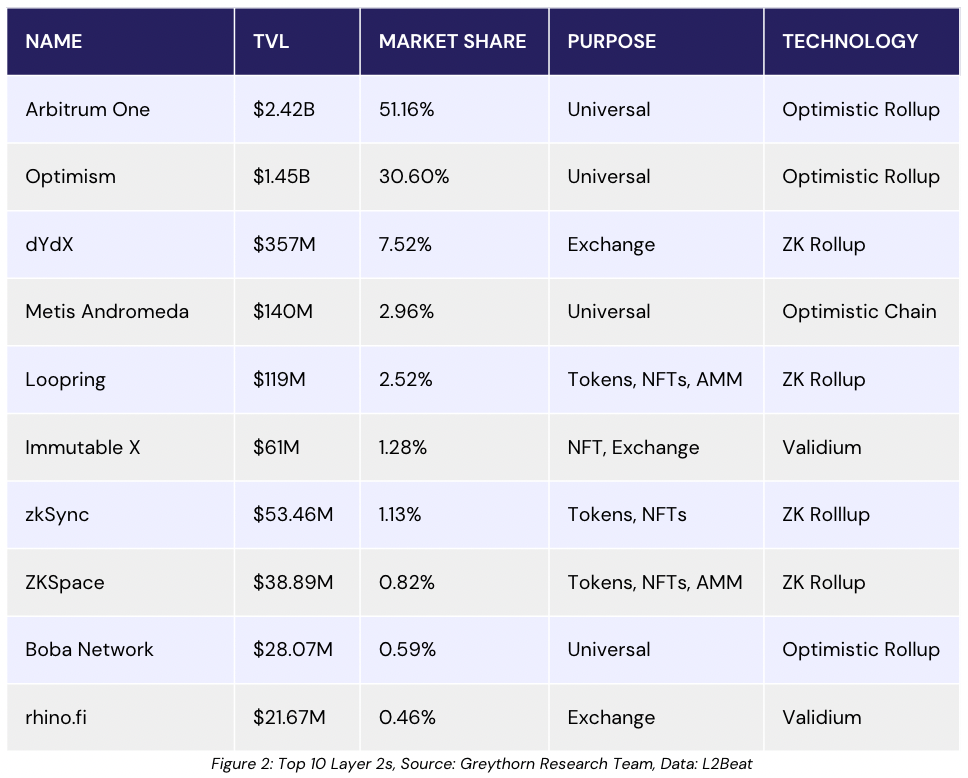

There are several layer 2 scaling solutions for Ethereum, including ZK-Rollups, Validium, Optimistic Rollups, Sidechains and Plasma Chains.

ZK-Rollups, Validium and Optimistic Rollups are the most popular solutions utilised across the current market. Optimistic Rollups hold a market share of 85.4% across the top ten Layer 2s.

ZK-Rollups and Optimistic Rollups are similar in that they both improve scalability by moving the computation of transactions off-chain & submitting highly compressed data to the mainnet. The differences are:

- Optimistic Rollups have greater potential in increasing scalability since they do not require complex cryptographic validity proofs.

- Optimistic Rollups have a far lengthier withdrawal horizon than ZK-Rollups due to their challenge period.

Onto StarkWare, Eli Ben-Sasson, the president, mentioned that the token is expected to go on-chain in October.

StarkWare was co-founded by Mr Ben-Sasson, the co-inventor of ZK-SNARK & ZK-STARK (an improved version of ZK-SNARK). It develops STARK-based solutions for the space. Their two main products are:

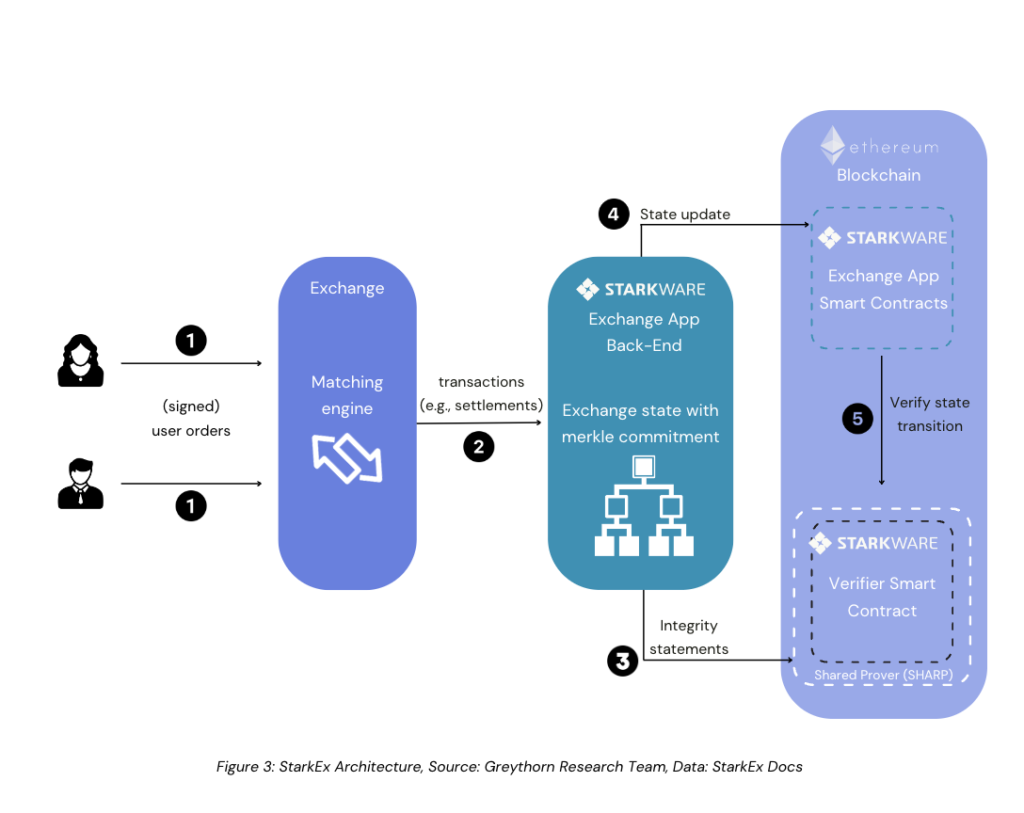

- StarkEx (Scaling as a Service):

- Provides customised layer 2 scaling services to dApps(B2B).

- Clients include dYdX & ImmutableX.

- Exchanges/dApps receive transaction details from their users and send them to StarkEx(Sequencer). StarkEx will convert byte-code from Solidity to Cairo and send them to SHARP (centralised shared prover by StarkWare) to prove validity. Once it is approved, it will be announced on the blockchain.

- StarkNet:

- A permissionless decentralised ZK-Rollup.

- It operates as an L2 network over Ethereum, enabling any dApp to achieve unlimited scale for its computation – without compromising Ethereum’s composability and security.

- StarkNet contracts & its OS are written in Cairo.

- Fees are collected from users for computation, storage, and transaction packaging. They pay the gas fee for uploading transactions to Layer 1. Sequencers can earn more by selecting transactions that pay more fees through an auction.

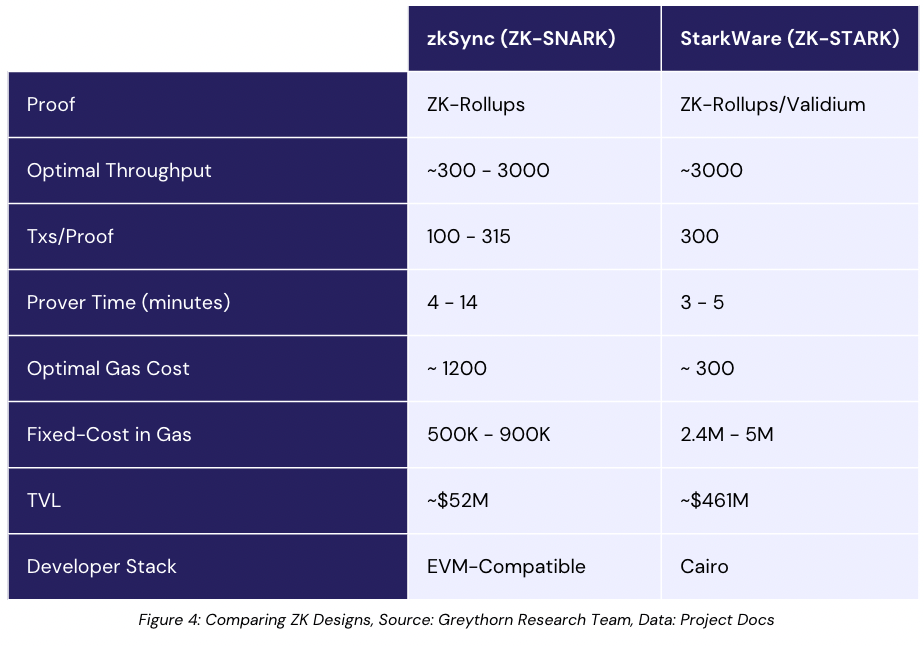

ZK-Snarks vs ZK-Starks

Decentralisation:

- ZK-SNARKs require an initial trusted setup phase to generate zero-knowledge proofs. Those parameters are usually held in the custody of a small group. Dishonest actions can occur.

- ZK-STARKs do not need the initial trusted setup and, therefore more decentralised & transparent.

Security:

- Since ZK-STARKs do not require an initial trusted setup, it uses a collision-resistant approach. It lowers the computation costs of ZK-SNARKs and makes ZK-STARKs unlikely to experience quantum computing attacks.

Scalability:

- ZK-SNARKs have a smaller byte size compared to ZK-STARKs. However, their computational demand makes them slower to generate proofs.

- ZK-STARK proofs also present a simpler structure in terms of cryptographic assumptions.

Comparable Analytics

Token: $STRK – StarkNet (To Be Released)

TVL: $461m

According to StarkWare’s Medium, the token’s use cases include:

- Governance;

- Compensation for contributors of the network and,

- Payment of fees on StarkNet.

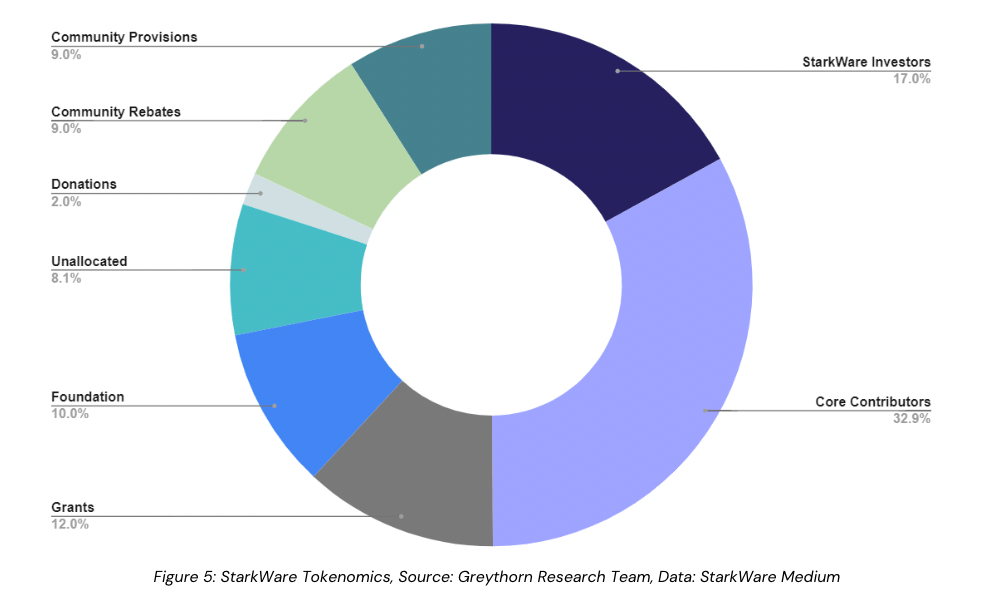

The total supply is 10 billion, with the potential for the protocol to mint more as decided by the community in the future. The details for the community’s allocation (50.1%) are:

- Grants (12.0%): Future research & development for the StarkNet protocol.

- Foundation (10.0%): Reserve to fund ecosystem activities.

- Unallocated (8.1%): TBD by the community to further support StarkNet.

- Donations (2.0%) To highly regarded institutions and organisations.

- Community Rebates (9.0%): To partially cover the onboarding costs from Ethereum to StarkNet.

- Community Provisions (9.0%): Compensation for previous developers and users of StarkNet. The snapshot was taken on June 1, 2022.

Bullish Fundamentals:

- Industry Growth: Ethereum has the largest market share by TVL (57.61%). The main problem of Ethereum is its scalability. Layer 2 scaling solutions can solve this problem. Layer 2 TVL increased from $51m in Jan 2021 to $4.68 in Oct 2022.

- Vitalik, co-founder of Ethereum, believes that ZK-Rollups are better over the long term than Optimistic Rollups.

- StarkWare has the most efficient ZK-Rollup technology on the market, co-founded by ZK-SNARK’s co-inventors.

- Compared to zkSync, StarkWare also supports Validium, allowing cost-efficient off-chain data storage.

Bearish Fundamentals:

- StarkNet’s biggest client, dYdX, decided to build its own chain with Cosmos’ SDK. It led to StarkWare’s TVL decreasing from >$1b to $461m.

- High Degree of Centralised Tokenomics, 49.9% of the token allocation is held with early investors and core contributors.

- Cairo is a new language which leads to greater difficulty for projects to deploy & transition their existing smart contracts to StarkNet.

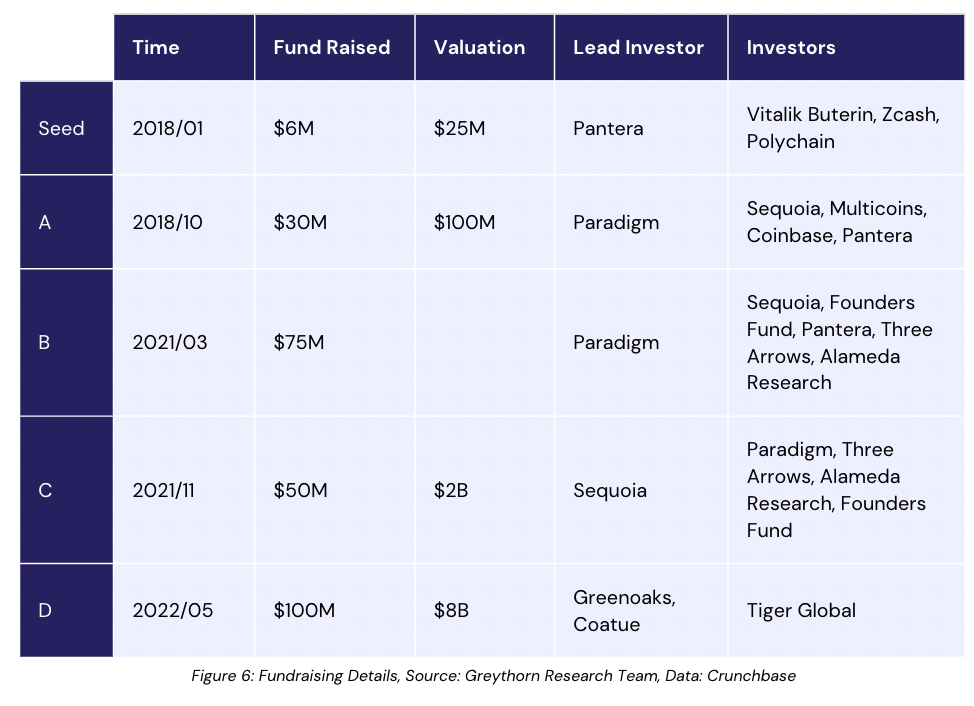

- After raising $100m in their series D funding round, StarkWare was valued at $8b in May 2022. Polygon is currently also valued at $8b, while it has $1.24b in TVL and a more mature ecosystem.

- Sequencers and provers are currently run by StarkWare, leading to centralisation concerns.

Closing Remarks

ZK-Rollups may not be new but are recently gaining increasing traction again as more projects seek to utilise their design. The launch of StarkWare has & still is being anticipated across crypto communities. Time will tell whether the ZK theme can grow & bolster crypto markets into innovation amid this larger bear market.

References

CoinGecko. 2022. Cryptocurrency Prices, Charts, and Crypto Market Cap | CoinGecko. [online] Available at: <https://www.coingecko.com/> [Accessed 29 October 2022].

CoinMarketCap. 2022. Cryptocurrency Prices, Charts And Market Capitalizations | CoinMarketCap. [online] Available at: <https://coinmarketcap.com/> [Accessed 29 October 2022].

DefiLlama. 2022. DefiLlama. [online] Available at: <https://defillama.com/> [Accesased 29 October 2022].

Frankenfield, J. (2021) ZK-SNARK, Investopedia. Investopedia. Available at: https://www.investopedia.com/terms/z/zksnark.asp (Accessed: November 4, 2022).

Homepage (2022) Starkware. Available at: https://starkware.co/ (Accessed: November 4, 2022).

Introduction (no date) Introduction :: StarkEx Documentation. Available at: https://docs.starkware.co/starkex/index.html (Accessed: November 4, 2022).

StarkWare industries – funding, financials, valuation & investors (no date) Crunchbase. Available at: https://www.crunchbase.com/organization/starkware-industries-ltd/investor_financials (Accessed: November 4, 2022).

The state of the Layer Two ecosystem (no date) L2BEAT. Available at: https://l2beat.com/scaling/tvl/ (Accessed: November 4, 2022).

What is StarkNet (no date) What Is StarkNet :: StarkNet documentation. Available at: https://docs.starknet.io/documentation/ (Accessed: November 4, 2022).

Wright, L.’A. (2022) Why dYdX is leaving Ethereum and StarkWare for a native chain on cosmos, CryptoSlate. Available at: https://cryptoslate.com/why-dydx-is-leaving-ethereum-and-starkware-for-a-native-chain-on-cosmos/ (Accessed: November 4, 2022).

Important notice and disclaimer

This presentation has been prepared by Greythorn Asset Management Pty Ltd (ABN 96 621 995 659) (Greythorn). The information in this presentation should be regarded as general information only rather than investment advice and financial advice. It is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. In preparing this document Greythorn did not take into account the investment objectives, financial circumstance or particular needs of any recipient who receives or reads it. Before making any investment decisions, recipients of this presentation should consider their own personal circumstances and seek professional advice from their accountant, lawyer or other professional adviser. This presentation contains statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Greythorn is not obliged to update the information. Those assumptions may or may not prove to be correct. None of Greythorn, its officers, employees, agents, advisers or any other person named in this presentation makes any representation as to the accuracy or likelihood of fulfilment of any forward looking statements or any of the assumptions upon which they are based. Greythorn and its officers, employees, agents and advisers give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this presentation. None of Greythorn and its officers, employees, agents and advisers accept, to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this presentation. This presentation is the property of Greythorn. By receiving this presentation, the recipient agrees to keep its content confidential and agrees not to copy, supply, disseminate or disclose any information in relation to its content withou