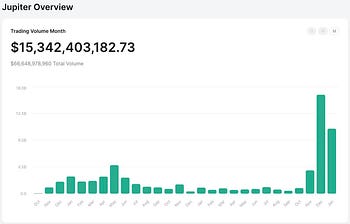

Project Name: Jupiter \ Network: Solana \ Project Type: DEX \ Ticker: $JUP Rank: #98 \ Market Cap: 718.6 M \ FDV: 5.29 B \ Circ. Supply: 1.35 B (13.50%) \ Total Supply: 10 B.

Opening Remarks

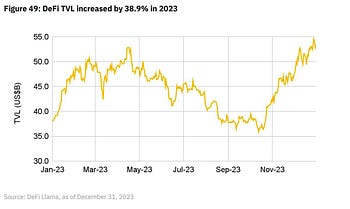

On January 15, 2024, the Binance Research team reported that the crypto market saw a remarkable recovery in 2023, with its total market cap surging by 109%. Similarly, DeFi experienced strong growth, with its total value locked (TVL) increasing by 38.9% from the previous year, reaching $53.4 billion.

Following the launch of its JUP token on January 31 and the overall resurgence in DeFi, Jupiter is positioned to be a significant player in the DeFi space on the Solana blockchain.

Project Overview

Jupiter began as an experimental project by a team dedicated to enhancing the utility of stablecoins within the Solana ecosystem. They achieved this by integrating with Mercurial and Serum, successfully launching Solana’s first cross-protocol liquidity swap. Motivated by this initial success, the team officially launched Jupiter as an independent project in November 2021.

To provide clearer context, DEX aggregators like Jupiter simplify the trading process. They do this by pooling liquidity from various decentralised exchanges to find the best swap rates for users. This approach is different from traditional DEXs, which depend on single liquidity sources. By comparing rates across multiple platforms, DEX aggregators minimise slippage and fees, making trading more efficient and user-friendly. This innovation tackles the issue of market fragmentation in DeFi, ensuring users get optimal trading conditions.

According to them, their mission is to build the most comprehensive and reliable swap infrastructure on Solana, catering to the needs of both individual users and projects. Jupiter introduces several innovative trading features to achieve this goal:

- Dollar Cost Averaging: This feature automates investing, allowing users to spread their purchases over time. It helps reduce the impact of market volatility.

- Bridge Service: They provide a bridge service that enables the transfer of assets between Solana and other blockchains, giving users access to a broader ecosystem.

- Perpetual Swaps: Jupiter offers perpetual swap trading, allowing for speculation and leverage on the price movements of assets without the constraints of expiration dates.

These features are part of their commitment to offering a seamless and advanced trading experience on the Solana blockchain.

Jupiter LFG Launchpad

Jupiter’s LFG Launchpad Beta represents a pioneering approach to supporting new projects, emphasising a community-driven and transparent model. The platform distinguishes itself by fostering long-term project success without the complexity of traditional launchpads. It relies on the open market and community engagement, avoiding complicated incentive structures and isolated price discovery.

Key to LFG Launchpad is its vast community support, customisable launch pools to counter bots, user-friendly design tools for liquidity management, and comprehensive trading features. This setup ensures fair price discovery and immediate liquidity, with enterprise-level support for technical aspects.

LFG Launchpad’s innovative mechanisms, including an equitable airdrop system and a dynamic liquidity market maker (DLMM), aim to provide a stable market entry for new tokens. By involving the community in the project selection process through DAO voting, Jupiter ensures that launched projects have robust backing and a clear path to success.

Tokenomics

Even though the Jupiter JUP token plays a pivotal role in facilitating governance within the ecosystem, granting holders the power to vote on critical decisions that shape the platform’s direction, JUP is not primarily utility-driven, as stated multiple times by its founder, Meow. From his recent words on a Reddit post:

“I believe that the idea that the utility of a token drives value is a myth created to justify why things have value or by project founders who are desperate to explain why their token has value. And I believe that most people couldn’t care less about utility, but rather they care about value,” Meow wrote, further discussing the notion on the Lightspeed podcast”.

“Over time, we will definitely want to allow JUP holders to be able to do a lot more with their JUP, including being involved in key ecosystem initiatives, etc., but that cannot be confused with why JUP is valuable,” he wrote.

Token Supply and Distribution

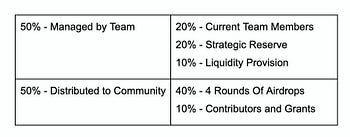

The total supply of JUP tokens is capped at 10 billion.

Team Allocation (50%)

- Team Members (20%): 2 billion JUP tokens are reserved for current team members, with a vesting period starting two years post-TGE, emphasising long-term commitment.

- Strategic Reserve (20%): Another 2 billion tokens are allocated for future team members, strategic investors, and stakeholders from past initiatives, held in a secure Team Cold Multisig wallet requiring a majority for transactions. These tokens are locked for a minimum of one year, with a six-month notice before any liquidity events.

- Liquidity Provision (10%): 1 billion tokens are designated for liquidity, managed through a Team Hot Multisig wallet.

Community Allocation (50%)

- Airdrops (40%): 4 billion tokens will be distributed to the community through annual airdrops, starting with 1 billion tokens at the initial event. The remaining 3 billion tokens will be stored in a community cold wallet, controlled by a 4/7 multisig.

- Grants (10%): 1 billion tokens are earmarked for community contributors via grants, managed by a community multisig wallet, with the Jupiter DAO overseeing allocation.

Initial Circulating Supply

The Genesis launch introduced an initial circulating supply of 1.35 billion JUP tokens, adjusted from the initially planned 1.7 billion. This adjustment encompasses tokens allocated for community airdrops, launch pools, loans to market makers, and liquidity provisions.

Growth Potential Outlook

The rapidly expanding DeFi market, along with Solana’s technological advancements, offers a promising environment for Jupiter to capture more market share.

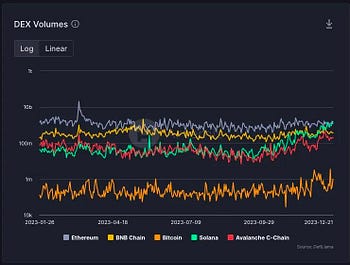

Solana’s recent accomplishment of surpassing Ethereum in weekly DEX volume in December 2023 cannot be ignored. As the first on-chain swap aggregator on Solana, Jupiter is strategically placed in an ecosystem that is not only drawing attention with high-profile projects like Render, Helium, and Hivemapper migrating to it but also reported a DEX volume that outpaced Ethereum’s, with Solana reaching $10 billion compared to Ethereum’s $8.8 billion.

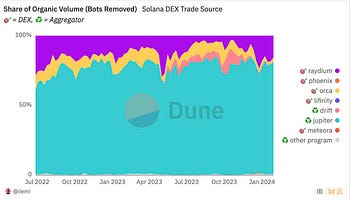

Being one of the most-used DeFi trading platforms by unique wallets across all major blockchains, and particularly on Solana where it directs 80% of organic volume and represents 65% of all volume, Jupiter has cemented its pivotal role within the ecosystem.

It would be fair to assume that the success of Jupiter is closely linked to Solana’s adoption. According to one of the latest Messari Solana reports, some major growth indicators were pointed out, including:

- Solana’s virtual machine (SVM) and general tech stack are gaining mindshare and adoption from outsiders.

- A 316% quarter-over-quarter increase in minted compressed NFTs (cNFTs).

- A rise in DeFi TVL to $368 million.

- Despite potential concerns, a 17% increase in market cap to $8.4 billion.

To explore additional Solana metrics, please consult the complete Messari report here.

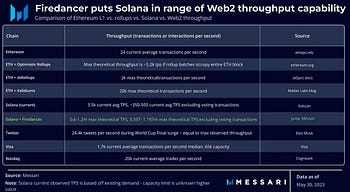

Additionally, the development of the Firedancer client by Jump Crypto, aiming for up to one million transactions per second, is set to significantly boost Solana’s scalability and performance.

This, along with the platform’s tech stack gaining traction among new adopters, suggests that with effective management, Jupiter is well-positioned for significant growth in the upcoming years, leveraging Solana’s technological progress and increasing market influence.

Competitors

Jupiter isn’t the sole thriving exchange within the Solana ecosystem; Orca and Raydium emerge as their principal competitors. Both platforms are DEXes built on Solana.

Raydium:

- Market Capitalisation: $260.11 million

- Rank: 188

- Fully Diluted Valuation (FDV): $564.27 million

- Circulating Supply: 255.76 million (46.08% of total supply)

- Total and Maximum Supply: 555 million

Orca:

- Market Capitalisation: $203 million

- Rank: 227th

- Fully Diluted Valuation (FDV): $411.10 million

- Circulating Supply: 49.38 million (49.38% of total supply)

- Total and Maximum Supply: 100 million

Orca has made a name for itself in the Solana DeFi sector through its user-friendly interface and the introduction of “Whirlpools.” These innovative pools provide concentrated liquidity, enabling higher yields for liquidity providers and offering traders improved pricing with minimal slippage.

Raydium, on the other hand, functions as both an automated market maker (AMM) and a liquidity provider to Serum, facilitating the integration of AMM liquidity with Serum’s centralised order book. This integration expands trading possibilities and enhances liquidity across the platform.

Orca seems to be primarily geared towards simplifying DeFi for the general user, making it more accessible and user-friendly. Conversely, Raydium targets advanced traders and liquidity providers, offering a suite of sophisticated tools and features designed to meet their needs.

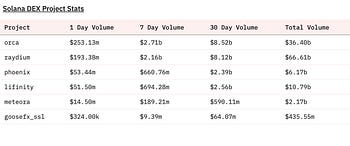

As of today, Orca has more market share in Solana DEX volumes at 48.6%, compared to Raydium’s 28.6%. However, Raydium leads in total volume with $66.6 billion, while Orca has generated $36.4 billion. It’s worth noting that Orca is a newer project but has shown impressive growth, generating $8.52 billion in the last 30 days compared to Raydium’s $8.2 billion.

Jupiter differentiates itself by pooling liquidity from leading projects like Orca, Raydium, and Drift. This strategy allows Jupiter to offer optimised trading strategies, ensuring users have access to the best exchange rates. Additionally, Jupiter provides a wide range of trading options and financial instruments through a single, easy-to-use platform, making it, perhaps, more convenient and efficient than either Orca or Raydium. On the other hand, Uniswap is the biggest DEX outside of the Solana network, famous for its high trading volume and large user community. Recently, Jupiter caught attention by beating Uniswap v2 and v3, with its daily trading volume going up by $10 million at the end of January.

Even with Jupiter’s impressive performance, Uniswap remains the leading DEX on the Ethereum network and DeFi, is known for its extensive liquidity and popularity among users. Hayden Adams, the founder of Uniswap, highlights the platform’s $700 million daily trading volume as proof of its significant influence. He believes Jupiter’s recent spike in trading could be more about short-term trading than a sign of lasting value.

Currently, both Jupiter and Uniswap have similar market values, with their FDVs ranging from $5 billion to $6 billion.

Bullish Fundamental Factors

- The increase in DeFi market dominance from 4.1% to 4.5% in 2023, along with the price recovery of DeFi tokens, creates a favourable environment for Jupiter to expand its volume into 2024.

- Ranking just below Uniswap and well above PancakeSwap in volume, Jupiter is established as the second-largest DEX on CoinGecko.

- Solana’s emergence as an “ETH killer” and its significant role in the DeFi sector boosts Jupiter’s potential for growth, given its status as the leading DEX aggregator.

- The LFG Launchpad showcases Jupiter’s commitment to innovation by improving launchpad functionalities and introducing new concepts, which draws a variety of projects and communities, further increasing volume and engagement.

- Meow, the founder of Jupiter, brings a wealth of DeFi experience, having advised major projects such as Kyber and Blockfolio, and co-founded wBTC. Additionally, the Jupiter team collaborates with a wide array of projects, showcasing a strong and diverse partnership network.

Bearish Fundamental Factors

- The functionality and reputation of the Solana blockchain, on which Jupiter relies, are critical. Recent and past network outages, including a significant one today and a near 20-hour downtime in February 2023, raise concerns about reliability. The frequent network disruptions question Solana’s claim to being a robust platform, impacting Jupiter’s ability to guarantee success in the competitive DeFi market.

- The sustainability of Jupiter’s technology within the DeFi sector is uncertain, given the dynamic and highly competitive nature of the industry.

- Post-airdrop periods often see a spike in speculative trading, increasing market volatility. This is compounded by scepticism from notable figures, like Uniswap’s founder, regarding the long-term viability of Jupiter’s trading volumes, which are believed to be inflated by airdrop-related speculation.

- The influx of meme coins and speculative airdrops within the Solana ecosystem adds to the uncertainty surrounding Jupiter’s short-term potential, indicating a risk-heavy environment.

Closing Remarks

At Greythorn, our work is driven by meticulous research, with a keen focus on on-chain analytics, liquidity movements, and unique proprietary data. If you find our insights valuable, we’d love for you to become part of our community. You can connect with us on LinkedIn, check out our website, or take a closer look at our X profile for deeper dives into the world of cryptocurrency.

We also encourage you to keep up with our latest research. This includes a detailed analysis of AI agents, powered by Autonolas, a comprehensive review of the Magpie ecosystem and its recent EigenPie subdao integration, and our monthly market update for January.

Disclaimer

This presentation has been prepared by Greythorn Asset Management Pty Ltd (ABN 96 621 995 659) (Greythorn). The information in this presentation should be regarded as general information only rather than investment advice and financial advice. It is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. In preparing this document Greythorn did not take into account the investment objectives, financial circumstance or particular needs of any recipient who receives or reads it. Before making any investment decisions, recipients of this presentation should consider their own personal circumstances and seek professional advice from their accountant, lawyer or other professional adviser. This presentation contains statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Greythorn is not obliged to update the information. Those assumptions may or may not prove to be correct. None of Greythorn, its officers, employees, agents, advisers or any other person named in this presentation makes any representation as to the accuracy or likelihood of fulfilment of any forward looking statements or any of the assumptions upon which they are based. Greythorn and its officers, employees, agents and advisers give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this presentation. None of Greythorn and its officers, employees, agents and advisers accept, to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this presentation. This presentation is the property of Greythorn. By receiving this presentation, the recipient agrees to keep its content confidential and agrees not to copy, supply, disseminate or disclose any information in relation to its content without written consent.