An exploration into cash-flow generation across DeFi & value accruals in the Post-Merge space.

The ever-changing landscape of DeFi has cycled from its early innovative years spear-headed by the likes of AAVE, UNI and COMP to food tokens attracting billions of dollars into a burgeoning eco-system. Rife with highly experimental and untested platforms, culminating in the liquidation of many institutions throughout the industry due to over-exposure and over-reliance on DeFi and leverage.

With The Ethereum Merge

kicking off, two major crypto narratives have started to pick up steam, namely;

1. Ethereum’s Merge narrative and distributed ledger technology projects that benefit from the switch.

2. DLT projects accrue more positive cash flow to its holders than inflationary emissions. They pay out such revenues in stables or blue-chip cryptocurrencies.

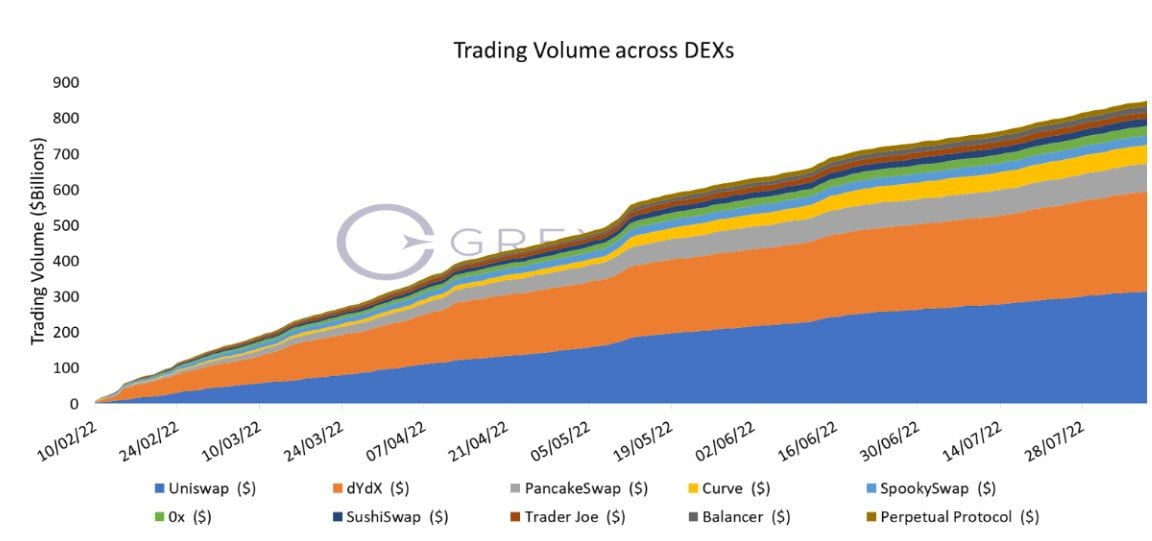

As we approach the merge, we find a considerable influx of trading volume in the DEX space, with $UNI leading the charge and $dYdX coming in second in trading volume.

Now that it’s #RealYield season, this fortnight’s piece will be delving into the various DLT projects and compare revenues along with valuations of a few prominent decentralised perpetual exchanges that readers should consider analysing as we come closer to the ETH merge.

Most leveraged trading occurs through popular centralised platforms that provide the best UX and UI. The question then arises, what are the benefits of decentralised trading platforms?

The main benefits and factors are the same as for most dApps:

- Self-custody of funds: Trading funds are not in custody by any centralised party, eliminating the risk of centralised control of user funds.

- Lack of KYC: By trading on decentralised exchanges, users do not require to pass any KYC/AML requirements, and the barrier to entering is the balance in their digital wallets and their choice of DEXs.

- Better Uptime: Due to being hosted as a smart contract on the blockchain, any DEX platform would benefit from a blockchain’s ability to stay online at all times. This is a significant advantage as centralised exchanges have historically shown to have untimely issues during periods of increased volatility and trading volume whilst dApps continue to perform consistently during the same timeframe.

The second quarter of 2022 has brought market uncertainty, dwindling interest in the ecosystem, and myriad repercussions in the market. Despite the turmoil in cryptocurrency and traditional asset classes, users would still trade and invest.

Users will still come despite the market cycles, and investors may still be able to profit through their activities on trading platforms. This source of demand is the prime driver of any trading platform. Whether trades are placed directionally or not, an investor could profit by investing in tokens related to said trading platforms.

Hence, we will compare three tokens within said space, namely $dYdX, $GMX, and $GNS.

dYdX

dYdX is a decentralised exchange specialising in derivatives trading, as suggested by its name.

Bullish Fundamentals:

-

Strong DEX Demand:

There is a demand to gain leveraged exposure to cryptocurrencies through perpetual contracts without losing custody/control of one’s own keys/ tokens. A DEX structure also allows individuals to engage in derivatives trading where it violates their countries’ laws (e.g. Australia does not allow retail investors to engage in futures trading on Binance).

-

Market Leader:

dYdX is the market leader in decentralised derivatives trading. It offers the best user experience due to its order book functionality and superior user experience. Furthermore, it offers lower fees than GMX.

-

Low P/E Multiple:

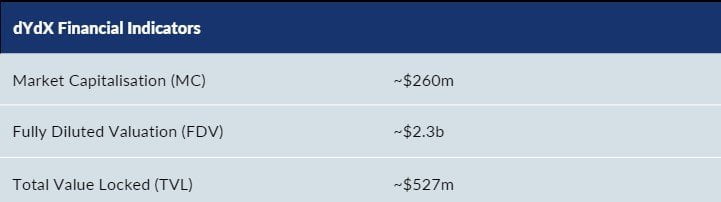

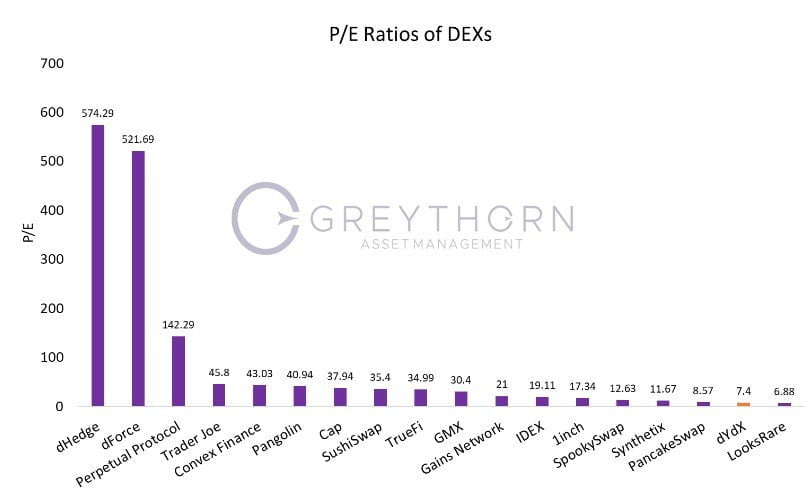

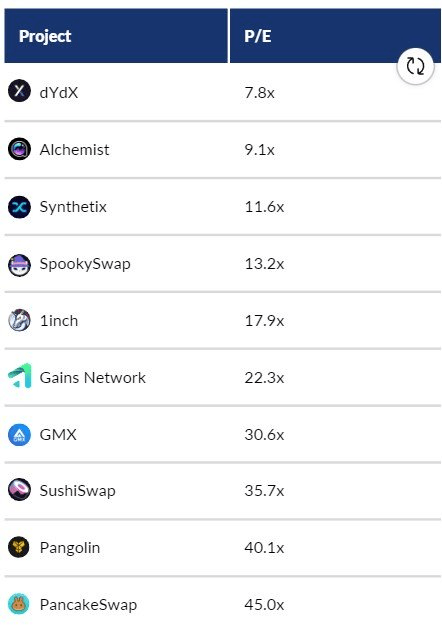

On a relative basis, dYdX is trading at a lower valuation than many of the dApps and dPerps tokens available across the market. dYdX trades at a P/E multiple of 7.4x, whilst their competitors are trading at a much higher valuation, indicating that the project may be undervalued.

-

Low Fees:

Traders have a low fee structure trading on dYdX. The market base fee is 0.05% and could go down with ownership of $dYdX. Their trading fees are comparable to larger exchanges such as Binance and FTX.

-

High Annualised Revenue:

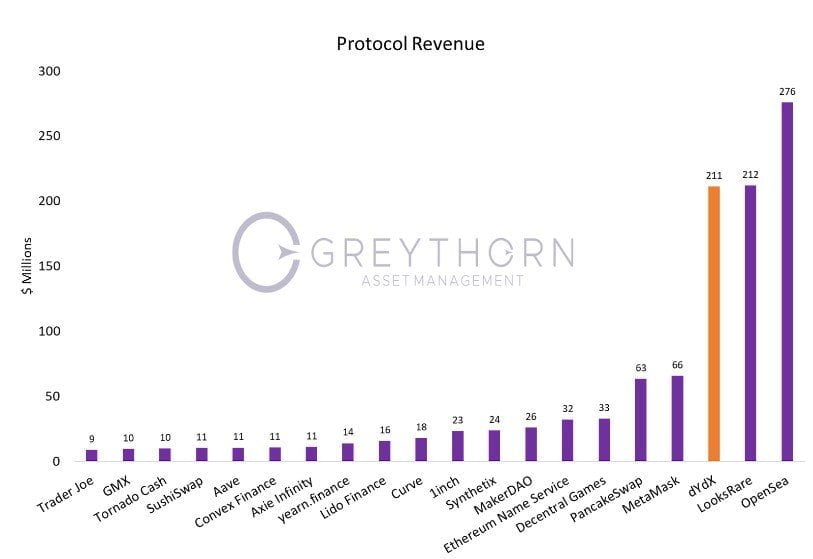

Being the largest decentralised perpetual exchange in the market, dYdX has a total annualised protocol revenue of $211.5M, placing it at 3rd place compared to other dApps.

Bearish Fundamentals:

-

Centralised Protocol Revenue:

Staking it does not provide a revenue share of fees earned on the trading platform. These go to the exchange as a separate entity or the traders/market makers themselves.

-

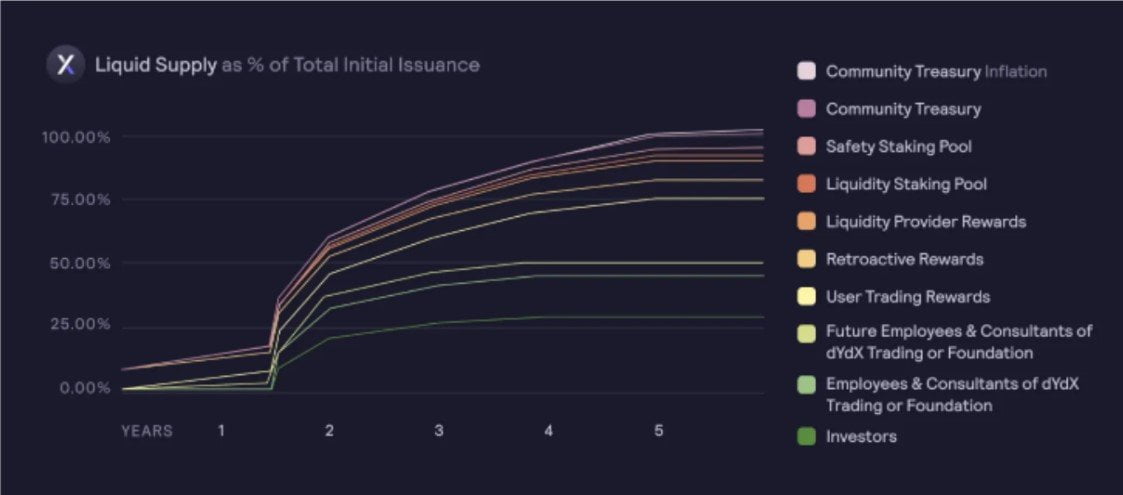

Highly Inflationary & Vesting Unlocks:

The continued inflation of the circulating $dYdX through liquidity mining for those trading on the platform benefits only the traders and the exchange at the expense of the token holders. Moreover, significant early investor unlocks are approaching, many of whom are in substantial profit and will likely choose to exit some of their positions.

What you can do with your $dYdX:

-

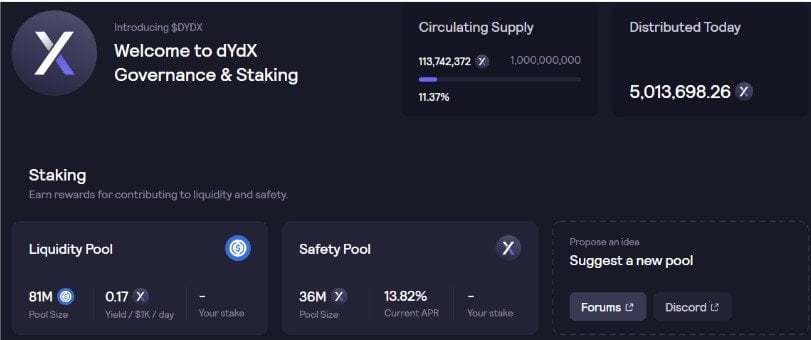

LP in Uniswap Pool:

$dYdX token holders could provide liquidity on UniSwap and earn 32% APR from trading fees. One disadvantage of this route is exposure to impermanent loss.

UniSwap Link:

https://info.uniswap.org/#/pools/0xd8de6af55f618a7bc69835d55ddc6582220c36c0

-

Use as Governance Voting:

By owning $dYdX tokens, users can vote on proposals that could alter the project’s course and trajectory.

dYdX Vote Link: https://dydx.vote/delegate

-

Stake in Insurance Module:

$dYdX token holders can stake their tokens within an insurance module, currently allowing the stakers to earn 13.82%. The drawback of staking in the insurance module is that tokens may be slashed due to a shortfall event.

-

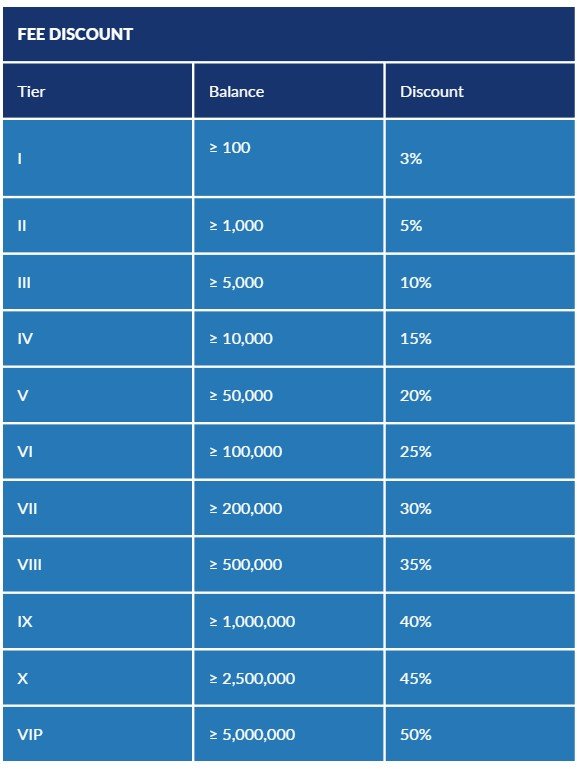

Trading Fee Discounts:

$dYdX holders enjoy a trading fee discount for any trades on the platform. This is another utility the token provides for community members who wish to trade in a low-fee environment on their platform.

GMX

A competitor to dYdX, GMX is a DEX that goes a step further and offers a decentralised order book.

With low swap fees and zero price impact trades, they support a unique multi-asset pool that provides liquidity providers and $GMX token holders fees from market making, swap fees and leverage trading.

Comparing this to centralised exchanges, DEXs hold less than 2% of the market share, which could rise as we see more activity on-chain due to the Ethereum Merge.

Bullish Fundamentals:

-

Strong DEX Demand:

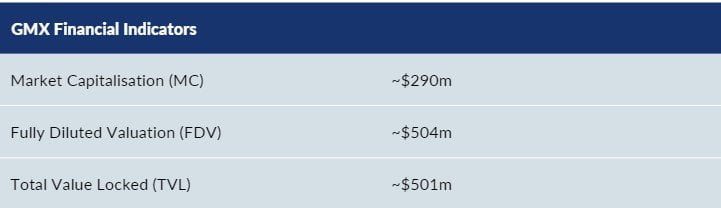

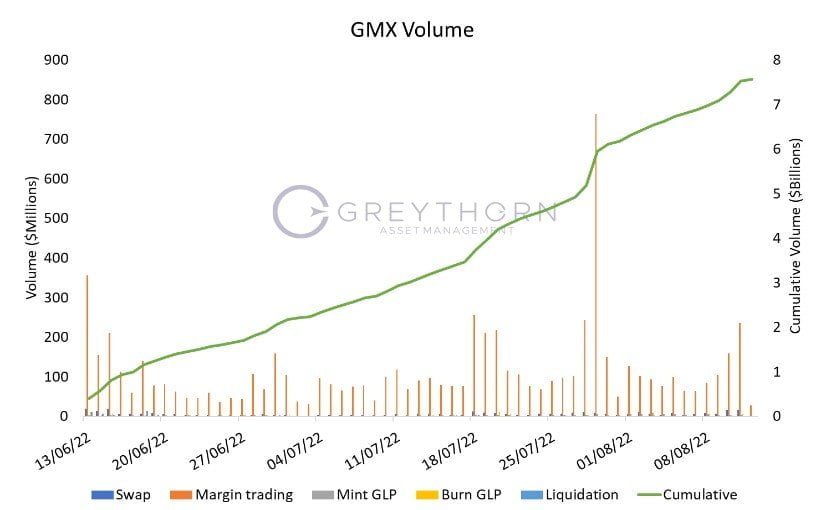

As mentioned previously, there is a strong demand for decentralised trading solutions for users. Their stats page shows their cumulative volume continues to rise despite the bear market cycle. Derivative volumes in traditional markets are typically far larger than spot volumes. If GMX could attain 50% of UniSwap’s volume in open interest, this would equate to $1.6m in daily fees, $584m annualised. GMX holders are entitled to 30% of these fees, which would be $175.2m. When you compare this potential future value to the current FDMC of $376m, the protocol begins to look incredibly cheap at just over 2x fees on a valuation basis.

-

Chain Agnostic:

Deployed on Arbitrum and Avalanche, the GMX platform itself has set a precedence that they are chain-agnostic, with plans to grow to new chains whilst also aiming to be the leader of the best-decentralised trading solutions for their users.

-

Strong Tokenomics:

GMX is the first mover to introduce two new tokenomics, namely their Multiplier Points (MP) and esGMX, to create a “sticky” demand and incentives for holding its governance tokens.

Multiplier Points:

Multiplier points are a way to reward long-term holders without inflation. Staked GMX

receives multiplier points every second at a fixed rate of 100% APR.

This, in turn, allows holders to receive protocol-generated fees in the form of ETH/AVAX as

each MP gives the right to a holder equal to a regular GMX token.

esGMX:

Once users receive esGMX via staking their GMX or GLP tokens, esGMX could be instantly

staked, representing the same reward mechanics as staked GMX – essentially entitling the

staker to ETH or AVAX rewards from platform fees.

Also, esGMX could be vested to unlock as GMX in one year. This is possible if a user locks their

GMX/GLP positions. The vested esGMX then unlocks linearly over one-year post-vesting.

Unstaking GMX or esGMX will mean a proportional amount of multiplier points are burnt,

incentivising holders to stake for longer to avoid losing their MPs. “For example, if 1000 GMX

is staked and 500 Multiplier Points have been earned so far, then unstaking 300 GMX would

burn 150 (0.3 * 500) Multiplier Points”.

Both these tokenomic factors provide “sticky” incentives for holders to stake their GMX for the

long term since the only way to acquire multiplier points is to accumulate them over time. This

also deviates from inflationary tokenomics as applied by many other dApp governance

tokens, whereby token supply gets inflated over time to liquidity providers/stakers such as

$AXS and various inflationary farm tokens that came up in 2021, such as $BUNNY, $CAFE

and even $CAKE.

-

Completely Decentralised and Low Fees:

GMX’s platform is the largest completely decentralised entity across its market, as dYdX utilises a centralised order book. GMX uses GLP, a basket of ETH, BTC, LINK, UNI, USDC, USDT, and FRAX to facilitate margin trading and swaps on the platform. Swaps are then executed based on pricing from Chainlink oracles feeding external sources, namely from FTX, Binance and others, which allows GLP to offer zero slippage swaps and low fees of 0.1% per trade.

-

Increasing Trading Volume:

dYdX currently records $2b in daily volume, whilst $GMX has recently reached a trading volume of 60% that of $dYdX. Based on the 30% fee entitlement, GMX token stakers would be entitled to an annualised $175m in fees. Comparing this to an FDV of $539m, its valuation begins to look relatively cheap at only 3.08x fees accrued.

-

High Staking and Whale Demand:

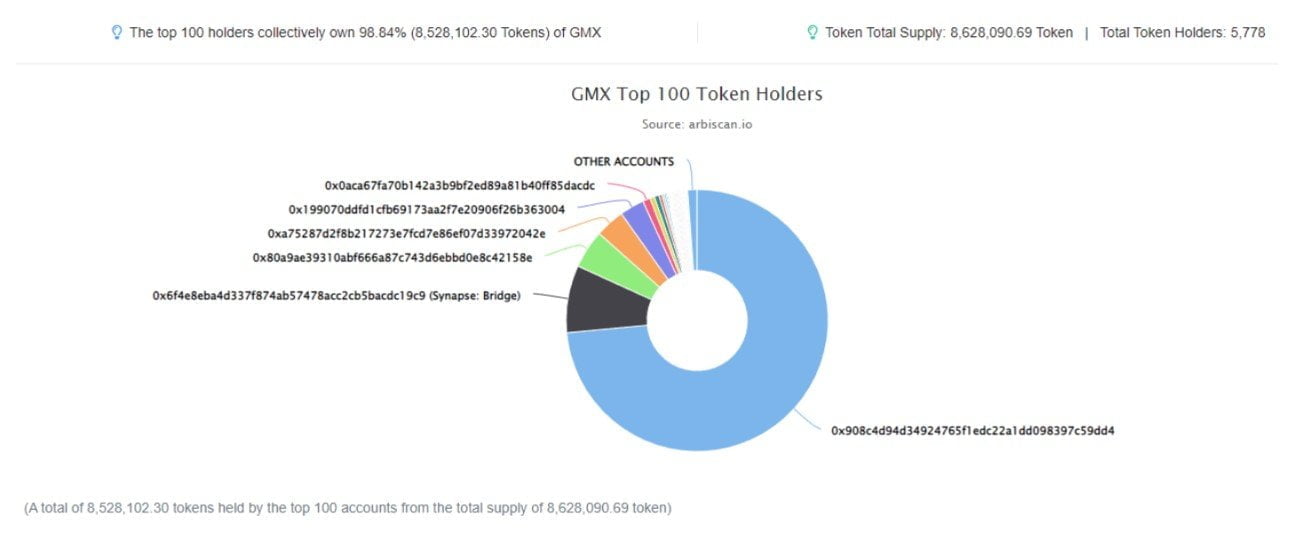

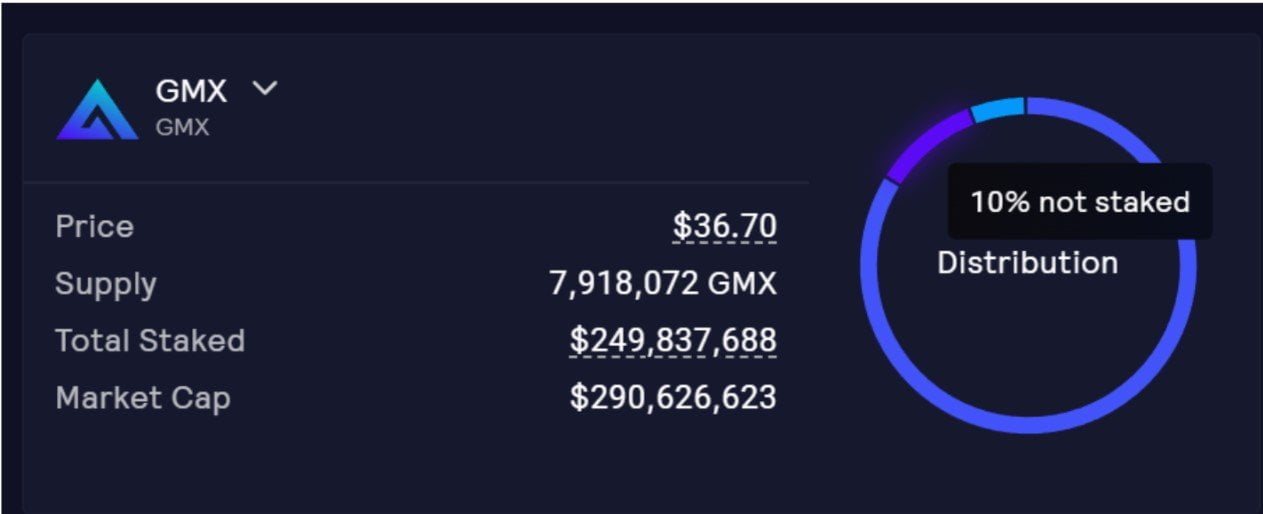

Looking into their token holding metrics, most $GMX holders (85% of total supply) have staked their tokens to earn fees off protocol revenue.

With just 5% in Liquidity Pools and 10% in circulation not staked, some evidence shows a high conviction for holders to hold for the long term instead of selling.

Bearish Fundamentals:

-

Higher Comparable Fees:

Potentially limited ability to capture most of the market due to its relatively higher fee structure. At 20 basis points, they are essentially 4x more than dYdX & up to 6.67x more than Binance (considering that BNB is used for fees). High fees will attract those willing to provide liquidity; however, there is no inherent advantage to using the GMX interface for your futures trading needs.

-

Inferior Interface:

Comparing interfaces, dYdX is superior. Its order book is more intuitive & user-friendly. This would deter traders from using $GMX compared to $dYdX and may hinder its growth on the user experience end of its expansion.

-

Limited GLP Trading Basket:

GMX only offers BTC, ETH, LINK and UNI perpetual contracts for trading. In contrast, dYdX offers 37 tokens across its ecosystem, and GNS provides a wide variety of asset classes ranging from forex, stocks and crypto.

-

High P/E Ratio:

Comparing the P/E ratio of $GMX to other comparable dApp tokens, we find that $GMX has a higher multiple than the market leader, $dYdX. Being at a higher multiple than earnings for the token, $GMX may be overvalued compared to its market peers.

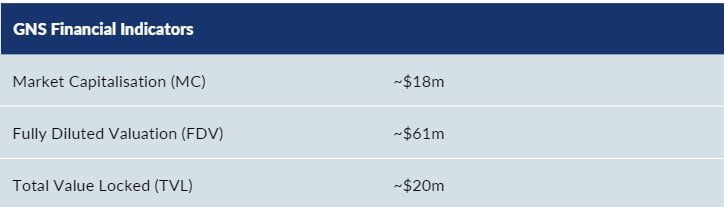

GNS – gTrade Platform

Gains Network offers decentralised trading with unique innovations such as decentralised oracles & zero funding fees. Its token supply is a function of traders’ success rates, now at 7.93%. The token essentially supports traders winning and will get burnt when they lose to balance out inflation & deflation.

Bullish Fundamentals:

-

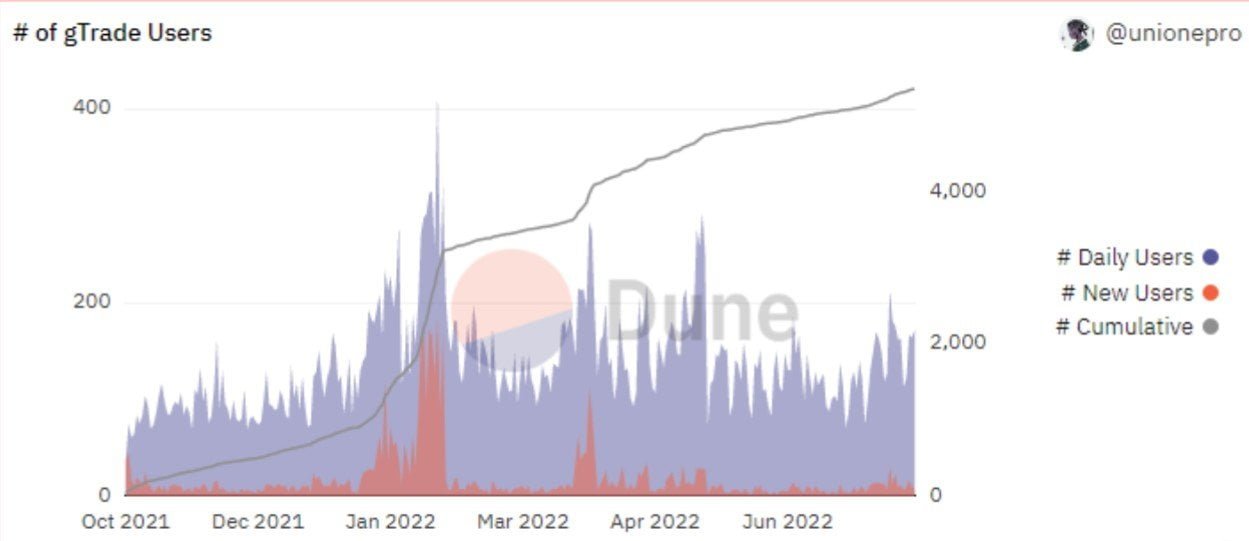

User Retention:

Based on the chart below, we find a strong user retention with daily users consistently using the platform, all the while the cumulative amount of users continues to rise throughout the past year of operations.

-

Wide variety of asset classes:

Decentralised access to asset classes ranging from traditional stocks & FX to Crypto and soon-to-be-released precious metals & agricultural perpetual futures.

- 48 crypto pairs at up to 150x leverage

- 10 forex pairs at up to 1000x leverage

- 25 stock pairs at up to 150x leverage

The protocol also plans to add features such as copy trading & trading competitions to appeal

to its large retail-focused community.

-

Low Fees:

The gTrade platform costs 0.06% for market orders (on opening and closing), 0.08% on limit orders for all cryptocurrencies, and 0.006%/0.008% for forex. The trading fee is applied when opening the trade and also when closing.

This is relatively competitive as we compare the fee structure to $dYdX, which was reasonably

surprising as a smaller platform. Their fee structure may be attractive even when compared

with centralised exchanges such as Binance and FTX.

-

Liquidity Efficient:

Due to utilising the DAI liquidity layer within its platform, gTrade has an advantage over its competitors in building order books for new pairs listed on their platform.

The platform also advertises that “by building a big DAI vault (with trading fee incentives),

every trading pair listed on our platform benefits from bigger position sizes and less slippage.”

This means the platform only requires DAI liquidity for ALL tradeable pairs.

Bearish Fundamentals:

-

Low Limit Restrictions:

Limits on how much collateral can be borrowed for higher value trades may keep whales away. Currently, the platform itself has several limitations to trading, namely:

- Limit of 3 open trades per trading pair per wallet.

- Maximum collateral per trade of 75,000 DAI.

- PnL on each trade’s collateral is capped at 900%.

-

Lack of Incentives:

Lack of additional incentives to trade on gTrade may limit growth vs a platform like dYdX that uses its token for liquidity mining (however, there are trading competitions with rewards mainly from Polygon’s ecosystem funds).

-

Currently Inflationary:

As mentioned before, the $GNS token is minted when traders win and burnt as traders lose. Currently, traders on the platform have been performing positively; hence, the $GNS token itself has been inflationary for the past few months. Nonetheless, about 25% of the supply has been burnt through organic deflation generated by gTrade, and potentially, as more traders lose, the $GNS token will transition back into a deflationary asset.

Closing Remarks

There are many different paths to development, both for how the exchanges function and how valuable their tokens will be. Web3 and the digital asset space is an ever-changing landscape, and it is impossible to conclude that $dYdX, $GNS and $GMX have reached their true potential and final form.

The development will continue, and their tokenomics will evolve as we progress over time. Nonetheless, the analysis above provides insight into these protocols, what users could expect and potentially do with these tokens, and how the ecosystem is ever-changing.

References:

App.gmx.io. 2022. GMX . [online] Available at: <https://app.gmx.io/#/dashboard> [Accessed 16 August 2022].

CoinMarketCap

Cointelegraph. 2022. Core Ethereum developer details changes to expect after the Merge . [online] Available at: <https://cointelegraph.com/news/core-ethereum-developer-details-changes-to-expect-after-the-merge> [Accessed 16 August 2022].

dYdX. 2022. Blog | dYdX . [online] Available at: <https://dydx.exchange/blog> [Accessed 16 August 2022].

Gains-network.gitbook.io. 2022. Fees, Spread & Example – Gains Network. [online] Available at: <https://gains-network.gitbook.io/docs-home/gtrade-leveraged-trading/fees-spread-and-example> [Accessed 16 August 2022].

Gains-network.gitbook.io. 2022. Home – Gains Network . [online] Available at: <https://gains-network.gitbook.io/docs-home/> [Accessed 16 August 2022].

Gmxio.gitbook.io. 2022. GLP – GMX. [online] Available at: <https://gmxio.gitbook.io/gmx/glp> [Accessed 16 August 2022].

Medium. 2022. Gains Network – Medium. [online] Available at: <https://gainsnetwork-io.medium.com/> [Accessed 16 August 2022].

Reddit.com. 2022. [online] Available at: <https://www.reddit.com/r/GainsNetwork/comments/r6izao/introduction_to_gains_network_for_traders_and/> [Accessed 16 August 2022].

Important Notice & Disclaimer

This presentation has been prepared by Greythorn Asset Management Pty Ltd (ABN 96 621 995 659) (Greythorn). The information in this presentation should be regarded as general information only rather than investment advice and financial advice. It is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. In preparing this document Greythorn did not take into account the investment objectives, financial circumstance or particular needs of any recipient who receives or reads it. Before making any investment decisions, recipients of this presentation should consider their own personal circumstances and seek professional advice from their accountant, lawyer or other professional adviser. This presentation contains statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Greythorn is not obliged to update the information. Those assumptions may or may not prove to be correct. None of Greythorn, its officers, employees, agents, advisers or any other person named in this presentation makes any representation as to the accuracy or likelihood of fulfilment of any forward looking statements or any of the assumptions upon which they are based. Greythorn and its officers, employees, agents and advisers give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this presentation. None of Greythorn and its officers, employees, agents and advisers accept, to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this presentation. This presentation is the property of Greythorn. By receiving this presentation, the recipient agrees to keep its content confidential and agrees not to copy, supply, disseminate or disclose any information in relation to its content without written consent.