At the beginning of 2023, the narrative of liquid staking was revived because of the Shanghai Upgrade. It is definitely good news for protocols like Lido, whose prices have more than doubled in 10 days since January 1st. In this article, Greythorn would like to:

- Introduce what the Ethereum Shanghai Upgrade is.

- Why the liquid staking protocols can benefit from the Shanghai Upgrade.

- The general impacts of the Shanghai Upgrade to the crypto market.

What is the Shanghai Upgrade

The Ethereum Shanghai Upgrade can be considered as a change in consensus mechanism of Ethereum from the technical perspective. According to the 151th Ethereum All Core Developers (ACD) call, Shanghai Upgrade is expected to be carried out by the end of March 2023.

This Upgrade will have three highlights, namely, the separation of code and data through EIP 3540 to simplify the transaction process, the withdrawal of ETH staked on the beacon chain, and gas fee reduction on Layer 2. Among these, the withdrawal of staked ETH has attracted the most attention and discussion.

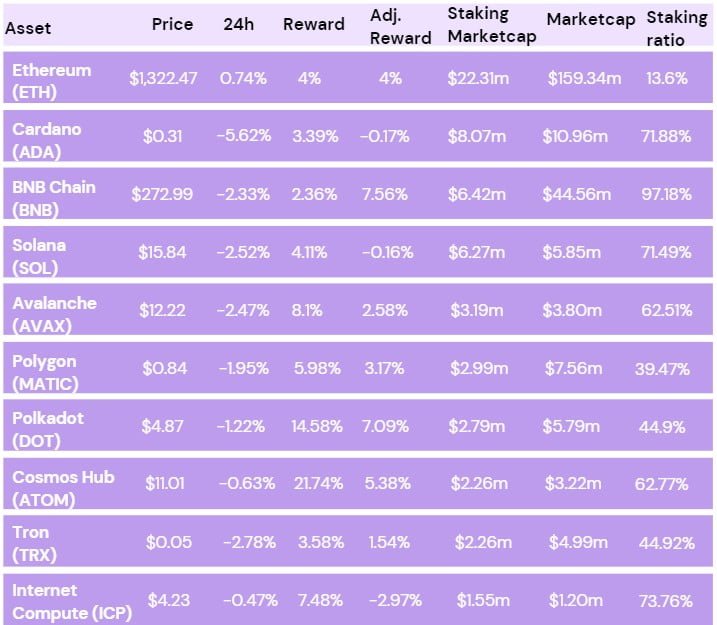

Ethereum completed the Merge in September last year shifted from Proof-of-Work (Pow) to Proof-of-Stake (PoS). Correspondingly, individuals are required to stake a certain amount of ETH to become validator nodes in the network. However, in the current architecture of Ethereum, the staked ET.H and rewards are locked, which directly affects people’s willingness to stake ETH Only ~14% of ETH supply has been staked, compared with staking ratios of more than 40% for the majorities of Layer 1s.

By allowing to unstake ETH, Shanghai Upgrade will greatly incentivize users to stake more ETH. Objectively speaking, the increase in TVL can also improve the security of the Ethereum network.

Liquid Staking Derivatives (LSD)

Although the Shanghai Upgrade is scheduled to go live in March this year, the market has already been hyping up for the related tokens. To understand the logic behind, we need to know the principle of “liquid staking derivatives (LSD)”.

Traditionally, the staked tokens under PoS will be stored in the escrow account for a long time. Therefore, if the staked ETH increases, which will accelerate the decrease of the tokens that can be used in DeFi protocols. Investors need to decide whether to stake ETH and earn rewards, or use ETH in other places (e.g. liquidity mining, lending, etc.).

If the options above are optimal? The answer is definitely no, since users have to take an opportunity cost no matter what, with capital inefficiency. To solve this problem, liquid staking derivatives (LSD) appeared in the market. It is a way to add flexibility of assets without losing the benefits of normal staking. Stakers will receive LSD 1:1 in exchange for the original assets, to represent their claim on the underlying pool and yield. LSD can be used elsewhere in DeFi, such as swapping, lending and using as collateral for borrowing. In other words, by investing in liquid staking protocols, users can unlock additional revenue streams apart from staking rewards. Thus, LSD seems to be a better choice.

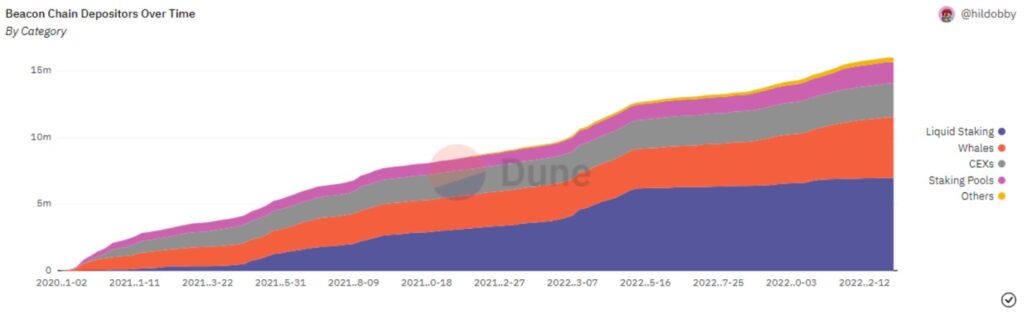

Clearly, many investors recognized this as well. From Dune Analytics, liquid stakers take the largest portion (32.8%) of all Beacon Chain Depositors and are still expanding.

Then, in the context of the Shanghai Upgrade, we can deduce the storyline of the entire narrative: First of all, the Shanghai Upgrade enables users to take out their staked ETH, people are more willing to stake. Instead of putting 32 ETH at least to stake on the beacon chain, liquid staking has zero barrier, and the fund can be withdrawn whenever stakers like. In result, ETH investors tend to choose the latter with stronger liquidity. Then, the enhancement of user base and deposit amount are essentially good for protocols, which will increase the expected revenue. Finally, token prices will rise given the fundamentals are sounds.

So far, we have sorted out the LSD narrative and why liquid staking protocols can benefit from Shanghai Upgrade.

The General Impacts of Shanghai Upgrade

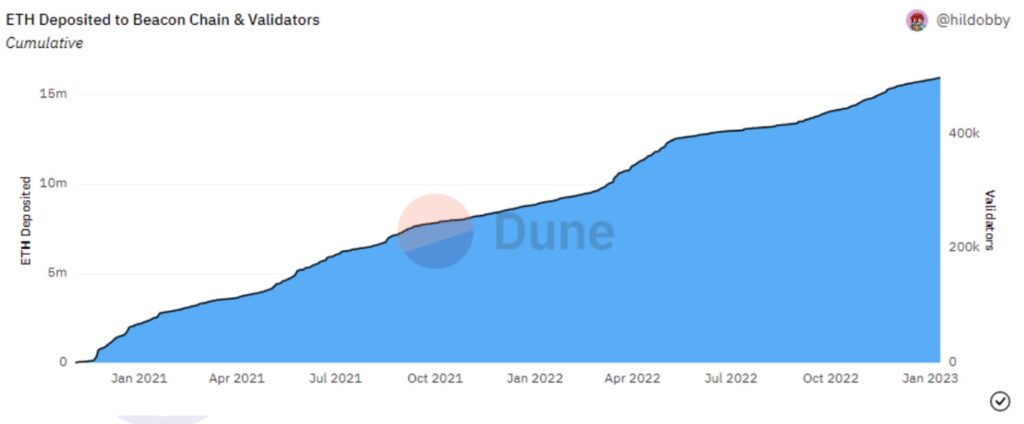

While we are experiencing the crypto winter, ETH staking is still an area of long-term growth. In 2022, the amount of staked ETH surged by ~80%, including ~15% after the Merge. Due to the highly distributed nature of its supply, the staking ratio of ETH may never reach the average staking rate of PoS network, 61%, but Shanghai Upgrade can be the main catalyst of the procedure.

More specifically, the potential impact of the withdrawal function in Shanghai Upgrade are summarized as follows;

1.Modest selling pressure of ETH

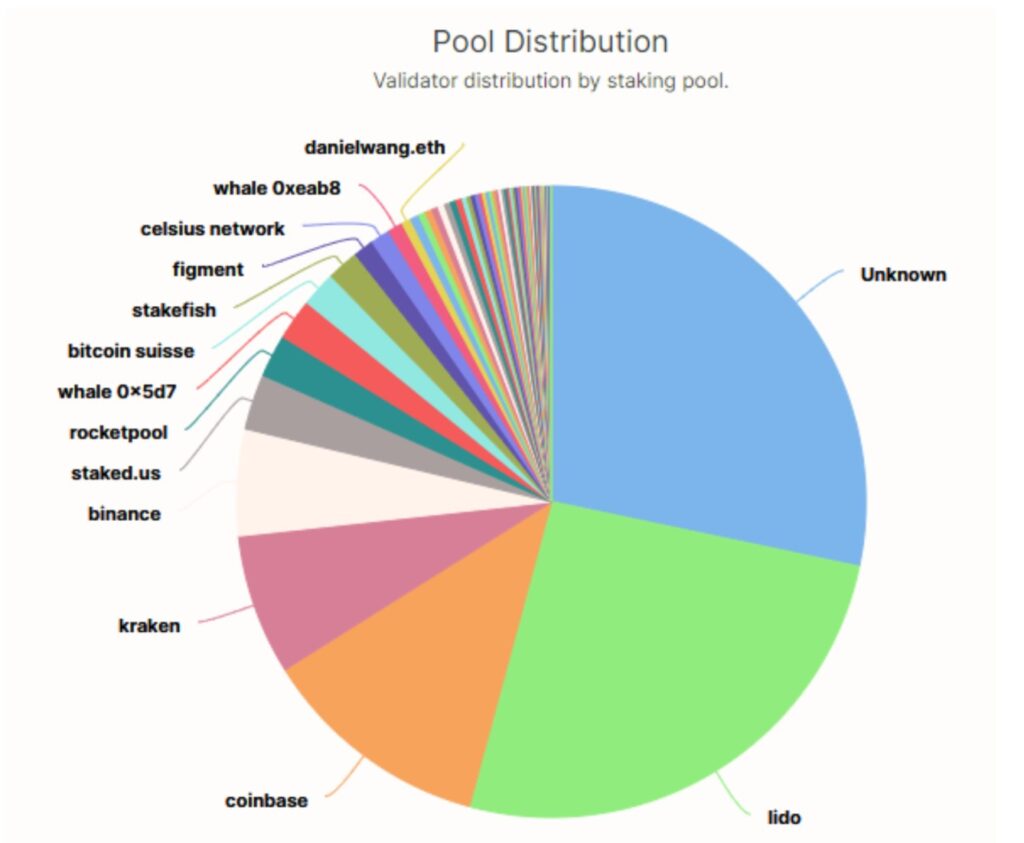

Among all Ethereum network validator nodes, apart from the unknown ones, the rest share-takers are all large staking service providers, or exchanges and mining pools, with Lido, Coinbase and Kraken as representatives. Hence, the selling pressure of ETH is assumed to come from these institutions.

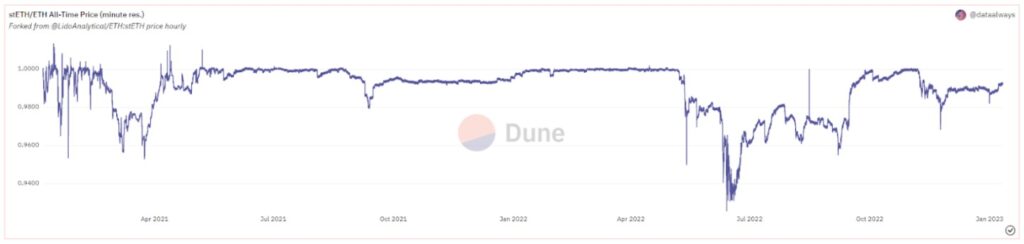

While, many of the organizations mentioned above have issued derivative tokens, taking stETH (Lido) and cbETH (Coinbase) as two of the examples. Roughly, the amount of LSD circulating in the secondary market has accounted for 44% (Dune) of the total staking. In the past two years, some of these tokens were discounted to different degrees. For instance, ankrETH was once -9% away from its peg in June 2022, and it has been a while for the gap between stETH and ETH, especially from March to June 2021 and from June to November 2022.

If we take a closer look at the price movements of stETH as the token with the best liquidity with the biggest market share, a lot of retailers deposited in 2020 or before have already sold their token holdings at market high before the first discount. As for the second one, the crisis of 3AC and FTX caused a massive outflow of institutional investors.

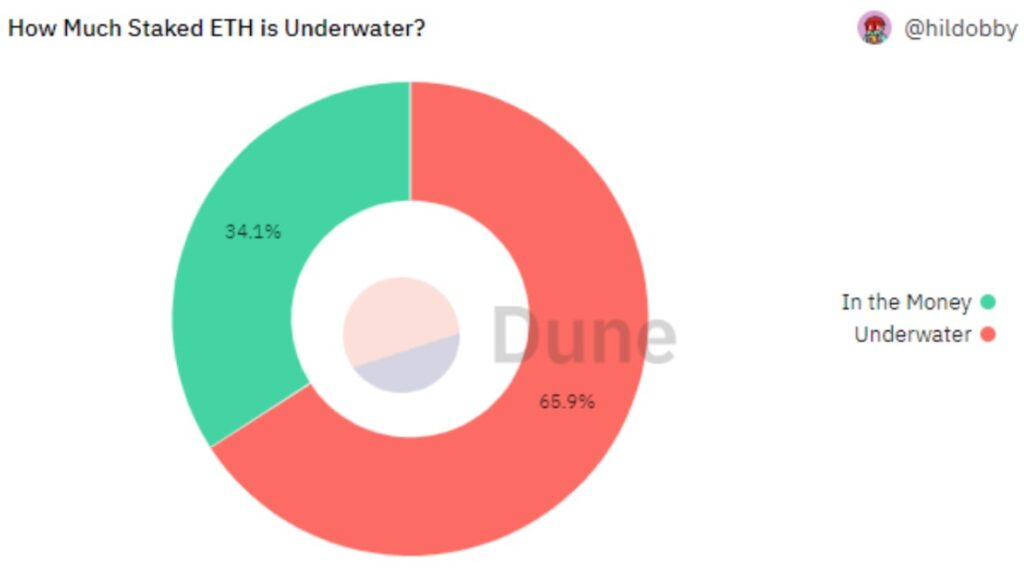

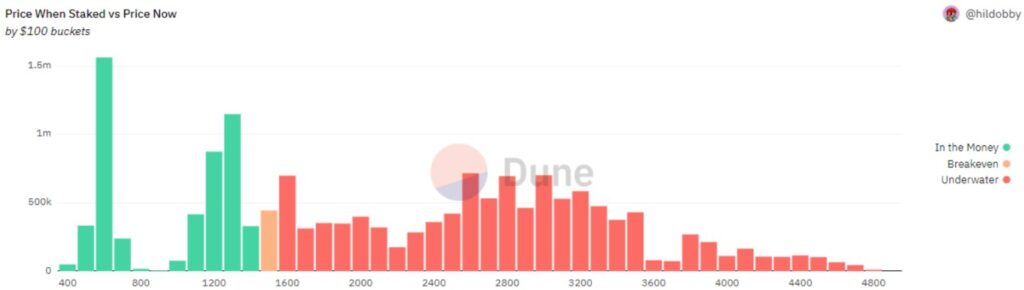

As per 20/01/2023, the purchasing cost of about two-third of ETH is higher than the current market price. Also, the cost of a large proportion of staking is $1,500 or more. In result, the fact that most of the staking is facing a loss may reduce the selling pressure of the market as well.

In a word, a bunch of capitals from liquid staking protocols already exited the market before Shanghai Upgrade. The cost of entry for ETH staking is also not low at all. There could be some price fluctuations by the news before the Upgrade, due to the existence of unrealized profit of the early practitioners. But it might be smoothed later on. This is primarily because the LSD in the secondary market is quite liquid with great demand, and the selling pressure has been somehow digested by the previous selling rushes.

2. Conducive to the value return of unpegged derivative tokens such as stETH

stETH is designed to be 1:1 exchange to ETH. Given that ETH can neither be unstaked nor collected rewards from the beacon chain, but sold through the secondary market, stETH has always been at a discount. Also, as a derivative of ETH with good liquidity, whales prefer to choose stETH as the exposure of ETH, which is another reason for the price volatility.

After the Upgrade, users can take their staked ETH back in several days, which is supposed to help with the value return of stETH and similar tokens. With the rewards 100% collectable, APRs of the liquid staking protocols can rise.

3. Arbitrage Opportunities before Shanghai Upgrade

If the protocols are safe, well-managed and reliable, it is of high probability that the price of the derivative tokens being deeply discounted will go back to 1:1. Cross-time arbitrage opportunities exist.

After showing the whole picture of Shanghai Upgrade and equipped our readers with how it impacts LSD and relevant protocols, we hope you have a better idea of why it is such a revolutionary change under heated discussion by crypto natives everywhere.

In the next article, Greythorn will dive into how LDO, RPL, SWISE and other native tokens from liquid staking platforms will be influenced and potentially react to Shanghai Upgrade.

Stay tuned and let’s continue the journey later!

References

- Ethereum (ETH) staking interest calculator (no date) Staking Rewards. Available at: https://www.stakingrewards.com/earn/ethereum-2-0/ (Accessed: January 27, 2023).

- Staking Pools Services Overview – open source Ethereum Blockchain Explorer (no date) beaconcha.in. Available at: https://beaconcha.in/pools#distribution (Accessed: January 27, 2023).

- Validator Balance Mean (no date) Glassnode studio. Available at: https://studio.glassnode.com/metrics?a=ETH&m=eth2.ValidatorBalanceMean (Accessed: January 27, 2023).

Important notice and disclaimer

This presentation has been prepared by Greythorn Asset Management Pty Ltd (ABN 96 621 995 659) (Greythorn). The information in this presentation should be regarded as general information only rather than investment advice and financial advice. It is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. In preparing this document Greythorn did not take into account the investment objectives, financial circumstance or particular needs of any recipient who receives or reads it. Before making any investment decisions, recipients of this presentation should consider their own personal circumstances and seek professional advice from their accountant, lawyer or other professional adviser. This presentation contains statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Greythorn is not obliged to update the information. Those assumptions may or may not prove to be correct. None of Greythorn, its officers, employees, agents, advisers or any other person named in this presentation makes any representation as to the accuracy or likelihood of fulfilment of any forward looking statements or any of the assumptions upon which they are based. Greythorn and its officers, employees, agents and advisers give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this presentation. None of Greythorn and its officers, employees, agents and advisers accept, to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this presentation. This presentation is the property of Greythorn. By receiving this presentation, the recipient agrees to keep its content confidential and agrees not to copy, supply, disseminate or disclose any information in relation to its content without written consent.